The age of Easy Money

Throughout the 1980s and 1990s, US recessions in industrial countries led to more-than-proportional recessions in EAC economies, but this link seem to have been broken in the 2000 during the US dot.com bubble.

When the global financial crisis hit the world in 2008 the only impact in Kenya came from the international banks which hold dollar deposits from Kenya. This risk could readily be transmitted to the banks in Kenya and finally to private sector firms and households.

But the impact in Kenya was limited because by 2008 foreign currency loans in Kenya accounted for under 10 percent of total loans, while deposits were about 13 percent.

So the bigger impact came from central bank which lost reserves partly as a result of shocks to the exchange rate and also due to stepped up demand for foreign exchange by risk adverse firms and households. Following the global crisis, the Kenyan shilling depreciated against the U.S. dollar by around 24 percent in the second half of 2008, as capital outflows increased but large privatization receipts from Safaricom boosted government deposits.

Plotting the Eurobond

To contain the financial crisis, the western governments took their taxpayers money and bailed out the bankers who had lost cash gambling on triple A- rated real estate that was actually being mortgaged out to borrowers who could not pay back.

After the dust of the financial crisis settled, the West went on a money printing spree which meant that easy money was looking for investment opportunities to gamble on.

Handed bailout money and promised long periods of low interest rates, the bankers were seeking highly rated investments to place the next bets, and most settled on African sovereign bonds that combined high yields with the relative safety of government bonds.

But the truth was that just like the mortgage backed securities home-owners in the US, African governments had no capacity to absorb the dollars let alone invest them in areas that could yield return quickly in a short time. Behind the rosy figures presented during roadshows propped by optimism of commodities markets were well connected predatory elites and their networks who would steal this money in gunny bags.

Before 2008, only South Africa and Seychelles had issued Eurobonds but over the next decade, 21 sub-Saharan African countries including Kenya had had more than one-dollar loan.

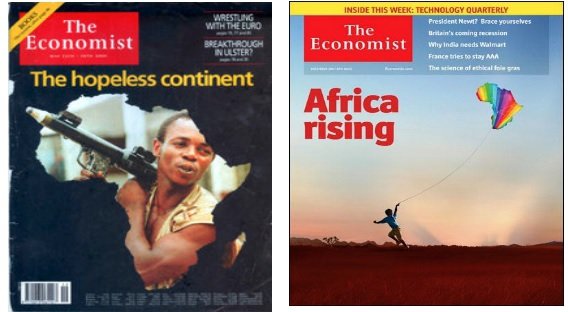

Africa Rising

The reason was simply the market had priced out African economies which were seen as too risky. PR campaigns to paint Africa rising narrative and push by IMF to guarantee currency risks opened up the market.

In Kenya the IMF was hawking Eurobonds as far back as 2009 even though the Fund admitted that Kenya did not need huge injection of dollars during the financial crisis.

Even though the IMF intervened at the time handing Kenya $200 million and SDR 135 million (or about US$200 million) during the crisis, a research on foreign currency by their own staff projected reserves at end-2009 would be relatively comfortable, even excluding the SDR allocations.

But when the IMF held a seminar to discuss the global financial crisis with Kenyan officials and later met to solidify the loan agreements including a change in the constitution to assure bondholders that Kenya will prioritize their debt over everything, they urged Kenya to issue a Eurobond to fund its infrastructure ambitions.

It is important to note at the time, in 2009 the Deputy Prime Minister and Finance Minister was Uhuru Kenyatta who would later become the President a few years later. Former IMF official Dr Joseph Kinyua, who would serve in his administration as the Head of Public Service was his Principal Secretary at the time.

“The authorities were considering staff’s proposal to move to a fiscal anchor of total public debt (including domestic and external), in light of increased external borrowing opportunities. Concerning a planned sovereign bond issue, the authorities agreed that its size, costs, and maturity profile needed to be carefully evaluated in order to mitigate potential risks” IMF Article IV 2009.

However, President Kibaki’s hesitation and unfavorable market environment led to the postponement of a planned sovereign bond issue and privatization.

Constitutional debt

It would however take years of reforms and a change in government to Uhuru Kenyatta who had been Finance Minister to actually issue Kenya’s maiden Eurobond.

Under the 2010 constitution Kenya debt would be charged on the Consolidated Funds Services which means that even if we were starving, hit by drought, floods or out of medicine, we will pay debt first before anything else.

Read also: How to be unemployed in 2024: Part III; The Kenya Kwanza’s Jubilee playbook

The technical advisors from the Bretton Woods institution also facilitated changes in metrics on Kenya’s debt from a fixed figure to a proportion of GDP and the IMF would assume the currency risk by providing a standby loan to boost Kenya’s level of reserves in order to help attract bondholders.

“The authorities have since allowed fiscal policy to be guided by a debt to GDP ratio anchor, and have updated the GAP,” Scott Rogers IMF representative to Kenya said.

The Jubilee tragedy

Some commentators believe the old Kanu slogan that they would rule Kenya for a hundred years had haunted the country with its former party members doing rebrands during every election and ruling the country with the same recycled elites in a series of coalition governments.

The rise of the Jubilee administration from Kanu’s youth wing on alliances to avoid responsibility for 2008 political violence was glossed over with the promise of grand projects.

The new administration announced they would deliver Vision 2030 through massive borrowing for dams, electricity, railways, roads and bridges.

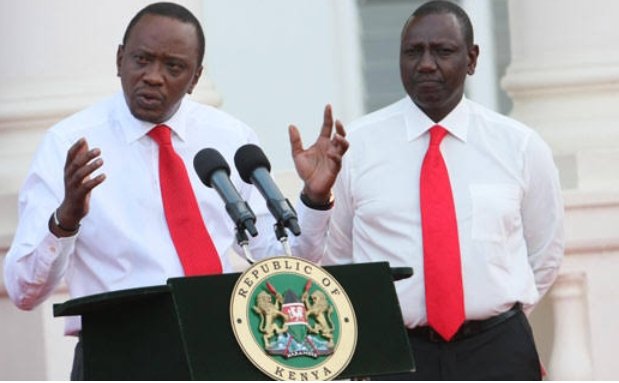

Donning matching ties President Kenyatta and his Deputy William Ruto appointed former IMF officials to handle monetary and fiscal policies including Dr Henry Rotich, Dr Patrick Njoroge and Dr Kamau Thugge and the late Geoffrey Mwau.

These would play key roles in Kenya’s new swanky status as a new client in the sophisticated Eurobond casino.

Geopolitical pawn

It was not only the Americans that were seeking a home for their dollars post 2008. The Chinese were seeking home for their overproduction of concrete and launched the ‘Going Out’ strategy just at the time President Kenyatta was being sworn into office.

By the time President Kenyatta came to power in 2013, in China, Xi Jinping had just risen to power and he sought to solidify the gains made during the Mwai Kiabki administration while entrenching his policy of debt funded, going out strategy.

Kenya signed a loan with China in May 2014 for the construction of the Mombasa-Nairobi standard gauge railway (US$3.6bn).

In the same year Kenya successfully tapped international capital markets with a debut US$2.0 billion Eurobond with demand from US investors dominating the issue with a share of 68 percent of total placement, followed by British investors with 25 percent.

Both loans were debt traps, the Chinese angling for Mombasa as one of its’ Strings of Pearls’ and America preparing Manda base to project control over the Indian Ocean and Chinese bound oil ships.

This loans blew Kenya’s debt out of proportion and with the competition in motion, like the cold war era, issues of transparency and accountability went out the window.

The Chinese loans was marked with corruption by state officials but at least delivered a money gobbling white elephant railway at nearly twice its cost.

Meanwhile Kenya has nothing to show for the Eurobonds which were to be used solely for development projects in infrastructure and energy, but when the money came part of it was diverted to pay for Anglo Leasing while the rest disappeared into budgeted corruption like NYS, Arror and Kimwarere dams.

IMF defended the diversion of this money as assuming minor liabilities, which for Kenya officials was a license for plunder.

“A conscientious preparation included making difficult decisions such as adapting legislation and assuming minor liabilities previously in litigation,” IMF Article IV 2014.

Read also: Selling an economy for trinkets Part III

Discover more from Orals East Africa

Subscribe to get the latest posts sent to your email.