Tax that paycheque

When I was young I sat in class and wondered how dumb my ancestors had to be to exchange their land, kin and elephant tusks for trinkets and alcohol.

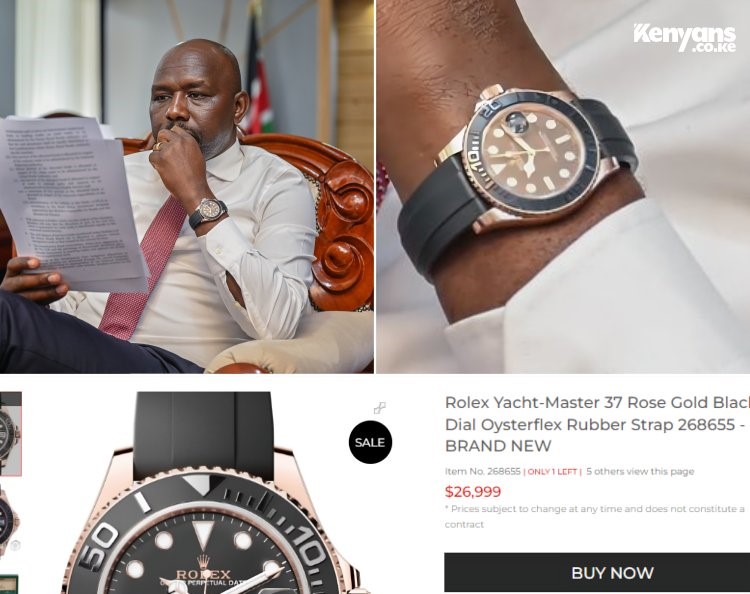

Then I grew up and witnessed my country sold for a printed piece of paper, wristwatches, belts and shoes and realized my children would ask the same question of me.

This is a story of debt and taxes and how real value, land, has been exchanged for illusions–like carbon credits, forex, conservancies and military bases in a country that is 80 percent desert.

Over the last decade as a business journalist, I have covered Kenya’s debt, experiencing first hand this phenomena, with extensive interactions with the actors, and a deep understanding on its evolution.

How the IMF in a bid to direct money printed in Western capitals to Africa to compensate for the zero interest rates created a debt bubble which now threatens to destroy East Africa’s largest economy.

Today my country is being torn apart by a polycrisis that has long been coming. The unfortunate violence by the administration is delusional, in imagining they can fix a sixteen-year-old problem with bandaid on bullet wounds.

President William Ruto came to power promising to wage a class war for the hustlers against the dynasties that had kept them poor.

This was the most taboo topic among Kenya’s elites who Daniel Branch in his book Kenya: Between Hope and Despair, 1963–2011 described as the multiplying ranks of the disaffected, the unemployed, and the poor.

When he came into office, he kept the promise, hollowing out pay slips of formal workers, ramming through IMF-driven tax policies that crushed the private sector. These are far-reaching policies that his predecessor, President Uhuru Kenyatta, had resisted for two years.

When he finally sought to tax cars, freehold land and bread of the #UpperDeckPeople, as one of his foremost economic advisors derisively describes the ‘spoilt’ middle class, every one of his well-laid-out fiscal consolidation plan came tumbling down like a house of cards.

The reason? Kenya’s high dependency ratio. For every middle-class President William Ruto gutted, a village was thrown back into poverty.

Now the hustlers, the middle class and the dynasties are all convinced that the political class that landed us in this ditch cannot be the one that will take us forward.

Legacy of debt

Kenya Kwanza’s administration may have hoped that they could manage six decades of suppressed class war by directing the anger of the country’s 19 million casual workers against about 2.9 million formal employees and using this to coerce consent for a multitude of taxes.

Formal workers carry the heaviest tax burden in the country accounting for nearly a third of the taxman’s income and have often riled against political choices made by rural and urban poor whose disproportionate turnouts sway elections.

On the other side are the casual workers emotively hating on their payslip neighbours urging the government to turn up the tax knob on the latter, thinking this will will not directly affect them.

But soon they, the casuals, or the hustlers as Dr Ruto would call them, would both realize they are in the same pot with the middle class. Where the middle class were hit by income deductions, the poor suffered from reduced consumption due to the reduced disposable income from the salaried workers. Moreover, even the casuals did not escape the taxman’s dragnet, paying higher consumption taxes such as valued added tax (VAT).

As companies collapse, banks are losing capital and the entire economy is bleeding jobs. The soaring ranks of the unemployed now find themselves without social support from a relative with a paycheck. Odd jobs such as washing clothes were easily available for the single mothers in the urban slums disappeared.

Gutting the young and the old

Unfortunately, this crisis runs deep. Moody’s’ downgrade of Kenya’s debt carrying capacity further into junk territory means that pension funds, banks and insurance are staring at unimaginable default event.

Over the last decade, Kenyans have become poorer and their savings have been dropping. Kenyans save only 12.1 per cent of their income which is lower than what we saved ten years ago, as cost of living rises faster than disposable incomes.

Also what the government has been calling growth has been inflation, which has wiped out half of the shilling value over the decade. A Kes1,000 note in July 2013 is today worth Kes548.60 in real terms, eroding the buying power of years of savings and pensions.

Many pensioners are finding themselves in rural areas with little more than they can afford to survive with some being forced to rejoin work as old watchmen despite to ease the burden of raising their children. An increasing horde of these senior citizens have sunk into alcoholism and depression amidst the crippling poverty.

The Irony is that ten years ago, Kenya marked its entry into the Eurobond market with fanfare, with the retired President promising borrowers lower interest rates as the government moved away from the domestic debt market and better exchange rates owing to the increased inflow of dollars from the issuance.

Neither interests nor exchange rates improved, and instead taxpayers are paying back the Eurobond through the nose. Kenya repaid that bond at twice its cost with nothing to show for it.

What’s more it has lost its sovereignty.

End of an economic cycle

Kenya is coming to the end of two decades of relative growth but reassessing outcomes it is doubtful whether over the period we have witnessed a change in fortunes.

Read also: How to be unemployed in 2024: Part I: Why the oracles are silent

Evidence shows that Kenya’s pursuit of economic growth, cash transfers, devolution and the package of structural adjustment programmes (SAPs) implemented now and in the 1990s have all failed to trickle down and multidimensional poverty and inequality remain as high.

Although promotion of overall rapid economic growth and the trickle down policies have been widely pursued as means of alleviating poverty and inequality, income inequality and poverty remained high even when the economy achieved relatively high rates of economic growth.

The IMF prescription

Kenya’s development had stalled for decades during President Daniel Moi’s autocratic regime whose rule relied on suppression and coercion. At the end of the cold war the West was no longer willing to fund corrupt dictatorships in Africa given the communist threat had been defeated with the fall of the Berlin wall.

To transition the governments into engines of economic growth, the IMF and its sister Bretton Woods institution the World Bank came up with the structural adjustment programme for Kenya and a poverty reduction programme but the Kanu government was too structurally compromised to implement such drastic reforms.

IMF in a 2001 Article IV review concluded little could be done with the Moi regime since the government simply could not meet conditions in reviews.

“An Enhanced Structural adjustment facility was approved in April 1996, but only the first disbursement was made, and the arrangement lapsed in April 1999 without completion of any reviews. The Poverty reduction and growth facility approved in August 2000 and augmented in October in light of severe drought expired without review,” said the IMF in a 2001 Article IV.

Kibaki Miracle

When the Narc Coalition government came into power, local and international players saw this as a golden chance for reforms.

Kenya accepted deregulation of the economy as proposed by the IMF agreeing to the obligations of Article VIII to maintain an exchange rate system that is free of restrictions on current international transactions and received IMF Support.

But pressing political needs to deliver on election promises saw President Mwai Kibaki raise salaries for civil servants and teachers and implemented the universal free primary education without having commensurate economic growth to support this.

The government needed money to fund this largesse and they turned to borrowing domestically which quickly became unsustainable. The Kibaki government then moved to lower the amount of cash reserve for banks at the Central Bank of Kenya which freed up resources for government to borrow cheaply and spurred consumption loans.

Unequal growth

This worked to push up inflation alarming the IMF but would also spur rapid private sector growth as the government implemented reforms that deregulated the market and encourage private enterprise.

“The wage bill is crowding out other spending and it will be a challenge to reduce wages as a share of the GDP over the medium term because of the announced salary increases for teachers and members of parliament and the consequential pressure to increase salaries of other civil servants,” IMF Article IV 2003.

It was obvious that growth through public service which in Kenya is typically ethnic would end up pushing inequality and would create a political nightmare as each tribe fought for control of the state which was ideally now the sole distributor of wealth.

While Kibaki’s policies spurred growth and spending delivering Kenya’s fastest economic growth in the years to 2007, his reluctance to push through constitutional reforms that could address long standing political problems soon proved that this road to prosperity had its limits.

A Damascus moment?

Kibaki, who had teamed with former Prime Minister Raila Odinga to end Moi’s 24-year rule, started having problems within his Narc coalition. Things got to a head when in 2005, a break-away faction of Odinga campaigned to defeat a proposed Constitution known as the Wako Draft, preparing the way for what would turn out into one of the bloodiest civil unrests in Kenya two years later.

When Kenya was hit by the 2007 post-election violence the realization that the rise from a low base and economic recovery was over, and had ended bitterly over inequality and tribalism.

consensus emerged of a need, not only for generating a bigger cake but also ensuring that every Kenyan participates in baking it and that it is also shared equally among Kenyans.

President Mwai Kibaki turned to the private sector, the National Economic and Social Council (NSEC). In a visit to Malaysia three years prior in 2015, this council was impressed by how a country that they considered similar to Kenya—from its ethnic diversity to its British-influenced institutions—had changed within a generation.

Although the group drew ideas from some of Malaysia’s policies, such as its focus on infrastructure, the main takeaway was the importance of creating a country’s national vision, the Visions 2030.

“At the beginning of the visit, Samuel Mwale who was an economist at the NESC said, “We had not made up our minds about doing a vision . . . [But] on Friday night, after our last briefing, we thought this thing could work,”

The McKinsey 1MDB draft

This vision had been developed with advisory from Boston Consulting Group and McKinsey & Company who both served as advisors to Malaysia’s Terengganu Investment Authority (TIA). This outfit would later transform into the infamous 1Malaysia Development Berhad (1MDB) Fund.

When in 2008 political rivals Raila Odinga and Mwai Kibaki agreed to share power and adopted the strategy, called Kenya Vision 2030, as a joint agenda; at the urging of some private-sector members of the NESC, the government contracted strategy consulting firm McKinsey & Company to assist.

Kenya’s top brains, industry giants, international experts from East Asia tigers and consultants for once made a deep dive into six sectors that had long been drivers of Kenya’s economy. They also looked for new opportunities based on global trends, like business process outsourcing and offshoring, a major industry in several high-growth developing countries.

More critical, they moved to open up the country, taking development to the far-flung areas that had initially been neglected by the economic policy of concentrating investments in the so-called high-productive regions by building roads, railway and airports.

Kenya aimed to reach middle-income status by 2030, but this needed much more money than the taxes that stood at around Kes300 billion could finance.

To solve this challenge, the agreement was that for the private sector would play the lead role, to put in substantial infrastructure investment as the government would push through structural reforms in the financial sector and on public financial management, governance, and trade policy.

But this would soon be abandoned and decision to fund this vision would be turned to debt, which had all of a sudden become cheap and abundant.

Read also: Selling an economy for trinkets Part II

Discover more from Orals East Africa

Subscribe to get the latest posts sent to your email.